Asset managers will have to forecast returns under distressed market conditions

Impact Institute’s Ruiz: Real value of firms not reflected in the books

Amid the pandemic-inflicted downturn, the real value of firms is under the spotlight. Adrian de Groot Ruiz, executive director of Impact Institute, explains how to find the real value of a firm when 50-80% of firms’ market value is not reflected in the books.

- Without the monetary tools to compare the impact of investments and companies, investors are flying blind

- Impact Institute’s integrated profit and loss statement monetises non-financial impact to allow financial and non-financial impacts to be compared in dollar-equivalent terms

- In terms of ESG ratings, good governance may help improve profitability and impact but is not profit or impact in itself

Social enterprise Impact Institute (II) focuses on the impact of financial activities, both positive and negative. Its integrated profit and loss statement (IP/L) seeks to steer companies, financial institutions and individuals on impact and provide an intuitive format to communicate the impact clearly to shareholders, stakeholders, the market and the economic landscape as a whole.

Spun-off the non-profit True Price, the institution’s impact framework intends to help organisations construct their own impact statements, setting their context and outlining the five key elements they constitute: the Integrated Profit & Loss (IP&L) Statement and its four derivatives, the Investor Value Creation Statement, the Stakeholder Value Creation Statement, the External Cost Statement, and the Sustainable Development Goals (SDG) Contribution Statement.

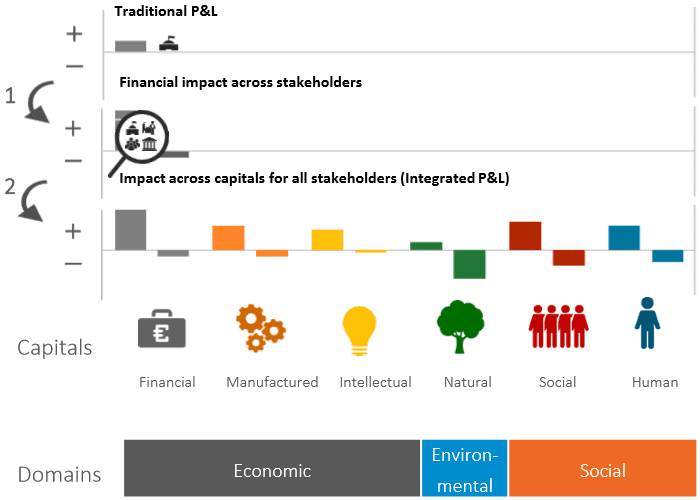

The methodology II employs assesses impact in a structured way using impact pathways that incorporate six capitals as defined by the International Integrated Reporting Council: financial, manufactured, intellectual, human, social and natural.

As such, the IP/L account extends the ordinary profit and loss (P/L) statement in two steps. First, it looks not only at investors, but at all stakeholders. Second, it measures not only financial capital, but all capitals.

The six capitals of investments representing the Economy, the environment and society

Figure 1. Two step extension of the traditional P/L into IP/L

Source: Impact Institute

These six capitals are measured according to key indicators. For example, payments from clients to the organisation in scope is a negative flow of financial capital, considering the perspective of the client and is recorded as a negative impact. On the other hand, filed patents are accounted as a capital flow in terms of the development of immaterial assets and technology and is recorded as a positive impact for the company in scope and investors as it creates future earning potential.

This monetisation of social and environmental impacts permits the development of effective risk-return-impact optimisation tools.

Impact Institute’s Executive Director Adrian de Groot Ruiz explained how investors and companies can benefit from using the IP/L, its advantages over ESG analysis as well as the wider industry developments:

Chris Georgiou (CG): We are seeing a growing number of high net worth individuals, foundations and family offices who very much want to increase their exposure to impact investing but are untrained or consider themselves unqualified to do so. How does Impact Institute engage with them and help them to consider impact?

Adrian de Groot Ruiz (AR): One of the key problems with impact investments is comparability and reliance on perceptions. Unlike the ability to compare the total expected return of a traditional portfolio, impact portfolios create a whole range of different impacts, such as green energy or poverty. There is currently no way to add up the total impact of a portfolio – so in a way, impact investors are flying blind.

Investors interested in impact have a lot of questions. We feel that if you don’t quantify and monetise that impact, you cannot have an answer to those questions. Our aim is to turn on the lights.

Our method of engagement is to help them in their impact journey and to understand the concepts. We identify their preferences in terms of impact, philanthropy and financial return. Then we can start optimising the impact of the portfolio, which can be done across the life cycle of the investment.

CG: Is the IP/L account produced as a periodic report, which is primarily backward looking, or does it have a forward-looking function?

AR: In principle, the IP/L, like a P/L, can be used to report historically whether that’s over a year or a quarter. The same method is also used if you are evaluating a firm forward-looking; if investors are considering various investment options, they can use the same machinery.

For example, if you want to have a positive impact on the climate, you can estimate for the next ten years how much carbon emissions will be saved in a certain investment, which can be discounted to the present. On top of that, every year, you can measure how many tons of CO2 have actually been captured out of the air and compare it with the estimates you made in the past.

CG: Would a client still need to have a traditional profit and loss sheet in addition to IP/L sheet to make a complete impact assessment?

AR: In principle, it is integrating traditional financial with non-financial impact. If you look at a normal P/L, you will look at the value creation on the bottom line for one stakeholder, which is the shareholder. The integrated P/L expands that in two ways by looking at all stakeholders. A wage is a cost for the company but a benefit for the employee; likewise, taxes create wellbeing for society. The second part is to also look at other capitals to get a complete picture of profitability.

The interesting part is that a multi-capital approach is also relevant to traditional financial investors. For example, if you look at the market cap of listed companies, 50-80% of market value is not accounted by book value on the balance sheet – it is the non-financial capitals such as intellectual and reputational capital, among others.

CG: The market has seen an explosion of ESG rating agencies for both companies and portfolios, Your IP/L product is a form of EES measurement, i.e. economic, environmental and social. What advantages does this EES assessment have over ESG – and/or should they both be considered?

AR: We think it’s about the economy, society and the environment. These three parts are fundamental. We see governance not as an impact but something that drives impact. Governance is not about intentions, nor about policies, it’s about affects. The IP/L has no line item for governance. Good governance may help you improve your profitability and impact but is not profit or impact in itself.

Secondly, many ESG ratings are largely based on proxies which do not quantify and measure impact. If you correlate normal financial indices – such as the ratings of S&P or MSCI on bonds – for example, they correlate above 90%. However, the correlation is very low for various ESG ratings. Rather than creating a score which is ‘good’ or ‘bad’, we work on open source standards and monetise it. Otherwise it would be the same as me coming to you with an investment proposition without the financial returns and just saying it’s a ‘7’ – it’s good. But what does that mean?

CG: Who are your customers?

AR: It’s quite diverse. One of our biggest sectors is financial services and we work a lot in the energy sector and with chemical companies. We also work with governments, as they have a large impact. Since last year, we have also been working with individual investors and related entities.

The difference is if you do an analysis of a bank or a listed company, it will be similar to the sector with standard economic and business data. For retail investors investing in new products such as medicine or energy, it requires a very specific approach.

CG: Would you say your model is a more a theory of change and logic model or an expected return model?

AR: It’s sort of a mix. Theory of change is more of a conceptual idea, as in what do you want to achieve and what actions do you take. We take that logic in an impact pathway, i.e. what are the activities that you do; what are the direct measurable outputs of that; what inputs do you use and what are the effects.

For example, if you invest $4 million in a company – either you had that money, or you borrowed the funds – so the inputs are the funds; then the output is the $4 million that you invest. Then you want to know what the impact of that investment is, i.e. how many tons of CO2 have I captured out of the air; how many people have I affected. But you must measure, quantify and then value the change that has been made – which allows for a calculation of return and comparison on investments.

CG: Impact Institute is one part of the entire impact ecosystem. What would you like to see from the industry as a whole and regulators to ramp up the size of the impact market?

AR: From the industry, we would ask for more long-term value creation. One actual example of an important impact mentioned by various experts and in our report to the United Nations was zoonosis. It now seems that the COVID-19 crisis was caused by zoonosis and is a negative impact of animal husbandry. If a business is more forward-looking, we believe you can better incorporate risks and opportunities.

We would like to see regulators asking organisations to publish their impact statements so they are transparent about their impact on society. Just as regulators ask listed companies to publish their financial statements to help markets function better, integrated statements will also help investors to steer on impact and long-term value creation.

Leave your Comments