Access to mobile banking in the Philippines remains exclusive and conventional despite a high mobile phone penetration rate. PayMaya is enjoying some success in penetrating the mobile banking space by reaching out to the "unbanked" segment, which makes up two-thirds of the population.

April 17, 2017 | Janine Marie Crisanto- Mobile banking penetration in the Philippines remains significantly low despite the increasing number of mobile phone users

- Paymaya has built a network of over 15,000 agents in the Philippines, higher than the largest bank network in the country

- Paymaya transactions reached $1 billion (Php50 billion) in the first quarter of 2016

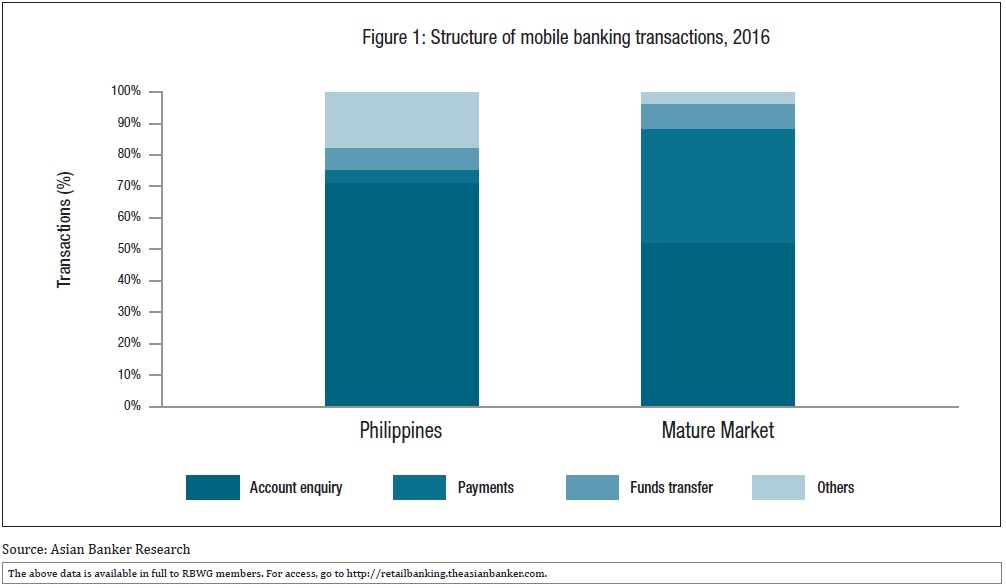

Although the Philippines has been recognised as one of the first markets to launch a mobile payment service 14 years ago called Smart Money, mobile payment propositions in the country still lag behind its global and regional peers. Mobile banking transactions are still heavily skewed towards account enquiry, while financial transactions such as payments and fund transfer are still minimal (Figure 1).

Compare to a mature market, payments in mobile banking transaction has not gained traction in the Philippines

Mobile banking penetration in the country remains low despite the increasing number of mobile phone users because of the underdeveloped information communication technology (ICT) infrastructure and the low level of smart mobile phone ownership. In fact, only 63.2% of Filipino mobile users have smartphones, which are compatible with advanced mobile applications. In addition, only 39.7% have access to the internet according to the 2015 state broadband report by the United Nations.

A number of advancements in the country’s mobile payments space came from telecom providers while most local banks chose to offer their mobile platforms as an additional service rather than a business generator. In 2002, telecom company Smart Communications (Smart) developed a short messaging system (SMS)-based fund transfer service named Smart Money under Smart Money Inc. In January 2016, the company was rebranded as PayMaya Philippines with a digital financial innovations unit called Voyager. PayMaya operates in three major spaces, namely: remittance (Smart Padala), prepaid online payments (PayMaya), and merchant acquisition (PayMaya Business). At present, PayMaya’s business is mainly driven by its remittance arm, and is still strengthening the issuance of the PayMaya cards and merchant acquisition.

Challenge

Mobile payments in the Philippines are usually tied to deposit accounts and credit card accounts. There are only 33.7 million deposit accounts or an estimated 50% of the adult Filipinos, which restricts the scale of mobile payment usage in the country. Furthermore, a rising number of tech-savvy millennials has resulted to a growing demand for online payment options. However, most of these young Filipinos who seek ways to consume digital goods are not yet qualified for payment products such as credit cards.

Given this small population and the difficult process of gaining a credit card due to the lack of a national ID system and the nascent credit scoring industry in the country, PayMaya saw an opportunity in launching a digital payment solution in September 2015, in the form of a virtual prepaid credit card, which does not require a bank account or other credit cards.

Product functionalities

In contrast to banks who have an average turnaround time of three to five days for credit card approval, PayMaya undercuts the conventional application process which requires documents such as proof of billing or income statement for its virtual credit card.

PayMaya users can access its virtual credit card by downloading the mobile application in Google Play Store or iOS App Store. Users have to register using the mobile app, which will provide them a 16-digit virtual Visa with a card verification value (CCV), which they can use to purchase goods online. In addition, PayMaya allows discounted inapp purchases of Smart mobile prepaid loads as well as peertopeer (P2P) mobile money transfers.

Alternatively, customers can also request for a physical card for offline purchases in supermarkets and malls, as well as to pay for transportation such as Metro Rail Transit (MRT) and Light Rail Transit (LRT). However, for users to enable their accounts for fund transfers and automated teller machine (ATM) withdrawals, they still need to upgrade their PayMaya account by presenting identification documents, as required by the Bangko Sentral ng Pilipinas (BSP), at upgrade centres or through a video call with a validation officer. This can be cumbersome especially there are only currently 50 upgrade centres available saturated in the greater manila region, therefore restricting the access to a physical card of Filipinos in provinces. Moreover, according to feedbacks on their Facebook page, validation via video calls are also reported to be inconvenient for some users because of the scheduling process.

Distribution network

In terms of loading money into an account, PayMaya has built a network of over 15,000 agents in the Philippines to make it more accessible and easier for its users to top-up their accounts. It also tapped BDO Unibank as its partner, allowing the bank’s customers to directly load money into the virtual card from their bank accounts for online and offline transactions.

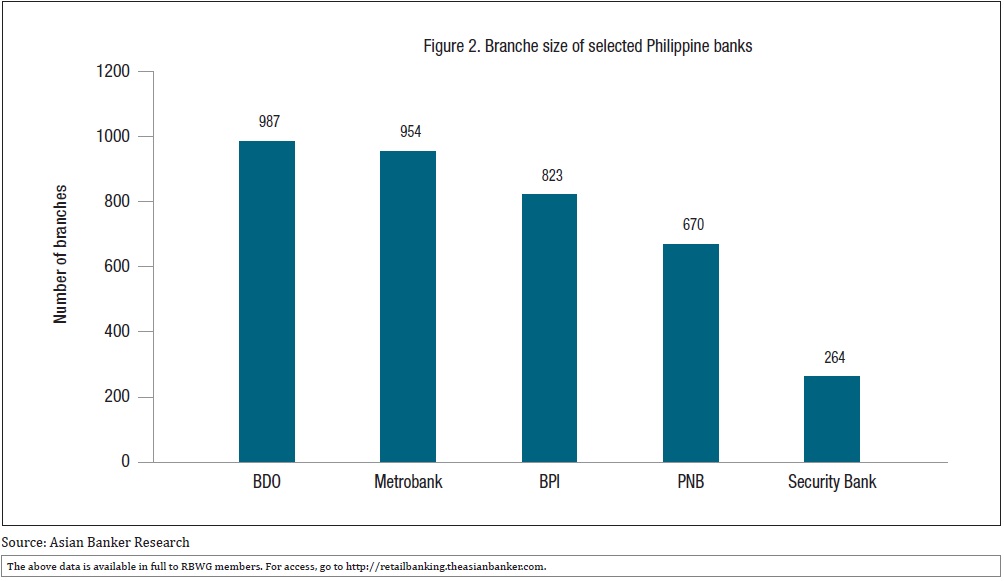

Leveraging on an agency model for its building its presence in the country, PayMaya surpasses the largest bank network in the Philippines – BDO’s network of 987 branches (Figure 2).

PayMaya does not only surpass the branch network of Philippine Banks, but also leverages on them in their agency model.

Security

As a BSP-licensed non-bank entity, PayMaya has leveraged on Smart eMoney’s platform, which is compliant with VISA and Payment Card Industry (PCI) data security standards. Aside from issuing physical PayMaya cards with EMV chip, it increases security by having transparency in purchases and alerting customers in case of fraudulent transactions. Transaction notifications are provided through SMS while transaction records can be viewed using the app.

Partnerships

Aside from partnering with local banks to offer its users more options for funding their accounts, PayMaya has also teamed-up with other fintech players globally to expand its customer base. In December 2016, PayMaya entered a collaboration with PayPal to allow users to withdraw their PayPal funds by connecting this to their PayMaya account. Moreover, through its partnership with Xoom, a digital money transfer provider, PayMaya has enabled almost two million Filipinos based in the United States to pay the Smart and PLDT postpaid bills of their relatives in the Philippines online.

Through collaborations, PayMaya strategically cements its presence in the everyday lives of the consumers, and helps boost the active usage of its product.

Business performance

After it was launched, PayMaya has emerged on top of the most downloaded financial services app in Google Play Store Philippines, surpassing applications from banks such as BDO Unibank and Bank of the Philippine Islands (BPI), and non-bank payment companies like GCash and PayPal.

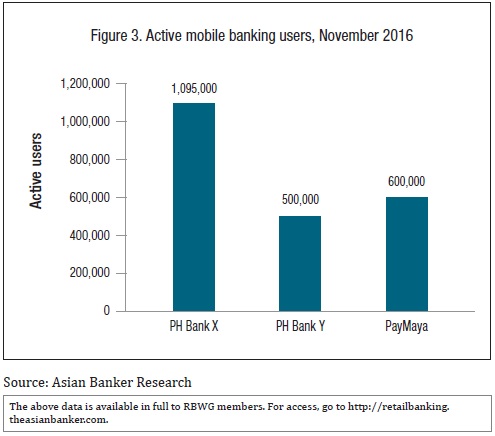

As of November 2016, PayMaya has over 600,000 active users, and it claims to have ended 2016 with a million – further closing the gap between their customer base with the volume of mobile banking users of the top banks in the country (Figure 3). In addition, the company reported that Paymaya transactions reached $1 billion (Php50 billion) in the first quarter of 2016, and it has aimed to meet its target of $4 billion (Php200 billion) by end of 2016. In line with this, 65% of PayMaya transactions came from online purchases as compared to the market average of 34% for prepaid cards – indicating the heavy usage of the card for payments.

In more than just a year, PayMaya has already acquired a mobile customer base size comparable to top banks in the Philippines.

Global comparison

Competition at the global level has become stiffer due to the increasing adoption of mobile payments with non-bank players stepping up and aggressively vying for customer share. Companies who were initially payments processors, social media platforms, e-commerce platforms, technology companies have penetrated the evolving mobile payments space to scale their businesses.

WeChat Pay

In Asia, the convergence of messaging platforms with micropayments proved to be a powerful combination. This is best demonstrated by the success of China’s WeChat e-payment services, which offers integrated wallet that is compatible with all phone operating systems. It has a staggering 300 million users as of May 2016 and has processed $550 billion worth of payments annually.

WeChat Pay tapped on the large network of users of WeChat’s messaging app, which latest statistics show at 700 billion – a number more than half of China’s total population. WeChat Pay has also taken advantage of various celebrations such as the Chinese New Year in 2014, pioneering digital red envelopes to boost its traction in the local market and attracting new customers. It also developed a public account whereby merchants can run promotional campaigns, undertake branding activities, and engage existing customers, who in turn help them reach potential customers through referrals.

PayPal

PayPal, whose payment ecosystem offers remittances, bill payments and reload, grew its overall revenue from $3.51 billion in 2010 to $9.25 billion in 2015 or a CAGR of 18%. The company aims to grow its PayPal wallet and offer consumer credit and payments services related to tax, education and health. The company has strengthened its relevance to both consumers and merchants by providing digital payment services using devices such as mobile phones, tablets, computers, and wearables gadgets. In 2015, PayPal launched One Touch payments, acquired remittance platform, Xoom, and entered into strategic partnerships with Facebook, Vodaphone, Alibaba, and other payment networks.

Paytm

Paytm, one of India’s largest e-commerce companies, has mirrored Alibaba’s business model. The company have raised close to $1 billion in funding, mainly from Alibaba in the end of 2016. It has also received the approval of the Reserve Bank of India to launch its payment bank.

Facebook has reportedly been expanding its payment services in Asia, which will allow users to pay for products listed on Facebook pages in a similar fashion as Wechat. According to reports, trials are being runin Thailand through Cash & Credit Card Payment Processor (2C2P).

The future

PayMaya has shown great potential in penetrating the Philippines’ mobile payments space despite challenges such as the archipelagic barriers, lack of a unified ID system, and underdeveloped ICT infrastructure. Although it is still at an expansion phase, PayMaya has leveraged on partnerships and roadshows to reach its target customers. Although it has yet to reach the level of global and regional mobile platforms and wallets in terms of services, functionality and traction, PayMaya has taken a step forward to reach the "unbanked" and "uncarded" Filipinos and contribute to the development of the e-payments ecosystem in the country.

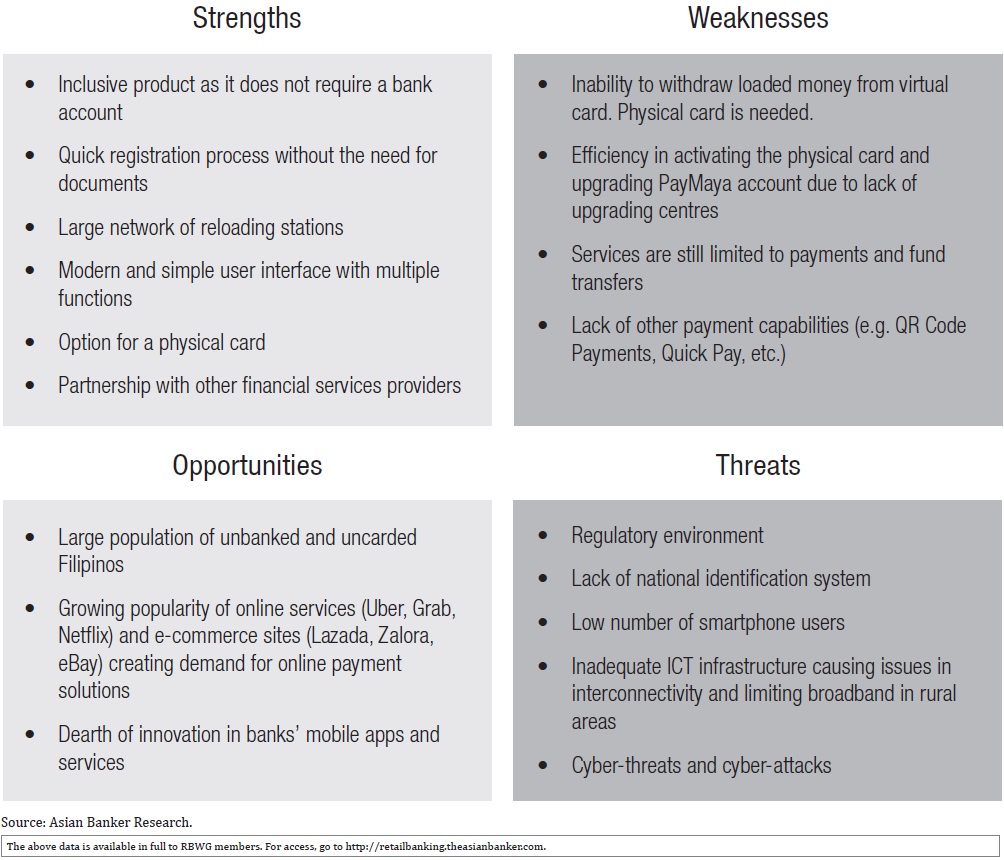

SWOT Analysis

Categories:

Payments, Retail Banking, Technology & OperationsKeywords:PayMaya, ICT, Mobile Payments, Credit Cards, Google Play, Branches, WeChat Pay, PayPal